Exploring how Aave's latest upgrade enables multi-configuration asset management and enhanced borrowing strategies

#Introduction

BGD Labs, a core contributor to the Aave protocol, recently implemented Aave v3.2, introducing significant updates to liquidity management within the protocol. The most notable feature is Liquid e-Mode, which enhances Aave's efficiency mode by allowing assets to participate in multiple configurations. With Aave v3.2 now live, the update removes previous limitations while opening new options for users. This article explores the practical implications of Liquid e-Mode, examining its benefits, trade-offs, and potential use cases. By analyzing these changes, we aim to provide a clear understanding of how Aave v3.2 impacts both users and the broader DeFi ecosystem.

#What is legacy e-Mode?

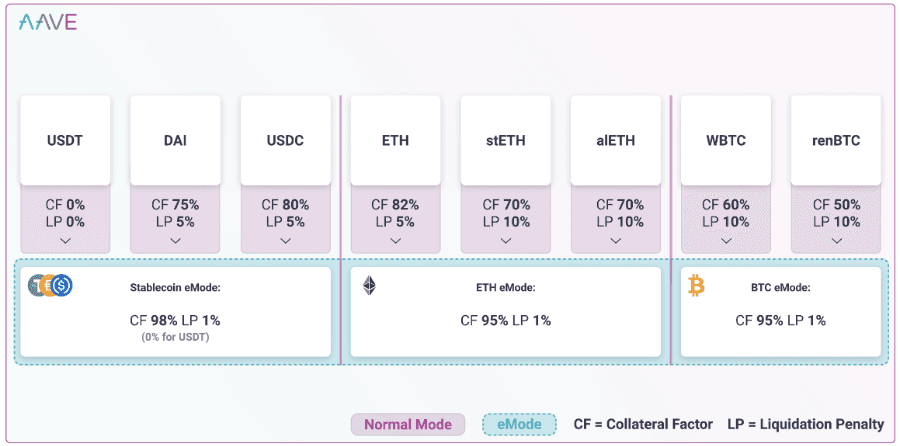

The initial version of e-Mode enhanced capital efficiency by applying tailored collateral parameters. These parameters allow users to borrow specific assets against others at higher loan-to-value (LTV) ratios when collateral and borrowed assets belong to the same e-Mode. Alongside increased LTV, e-Mode raises the Liquidation Threshold (LT) and reduces Liquidation Penalties (LP), making borrowing more efficient. These benefits are limited to groups of correlated assets, such as stablecoins, ETH and its Liquid Staking Tokens (LSTs), or BTC wrappers, where price deviations between assets remain minimal. This ensures enhanced efficiency and does not introduce excessive risk.

Source: Example of e-Mode setup - Aave 3.0 Whitepaper

Legacy e-Mode was introduced in Aave v3.0. Aave's v3 technical paper explains how e-Mode enhances risk management by enabling efficient strategies like yield farming within correlated asset groups. Through category-specific oracles that stabilize pricing within these groups, e-Mode reduces the risk of unnecessary liquidations from minor price deviations. Users must close any non-e-Mode borrowing positions before entering e-Mode to ensure compatibility with its parameters.

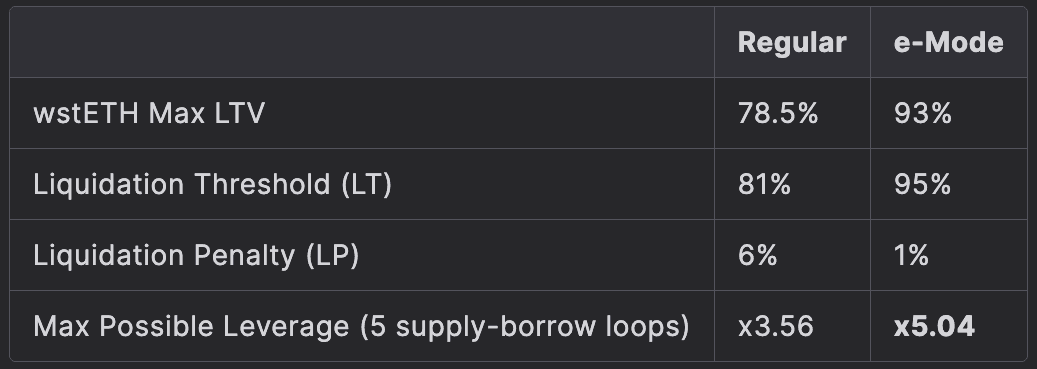

E-Mode is commonly used with correlated asset pairs, typically where the collateral is a yield-bearing version of the borrowed asset (e.g., wstETH supplied as collateral to borrow WETH). Since these correlated assets usually move within a narrow price range, the liquidation risk when borrowing against them is lower. Aave uses Correlated Asset Price Oracles (CAPO) to protect users from unexpected price deviations between assets and their staked versions by implementing upward price deviation safeguards.

For example, in Aave v3's ETH-correlated e-Mode, assets like WETH, wstETH, weETH, rETH, cbETH, ETHx, and osETH receive enhanced efficiency parameters. This configuration enables users to achieve higher leverage when borrowing against assets like wstETH.

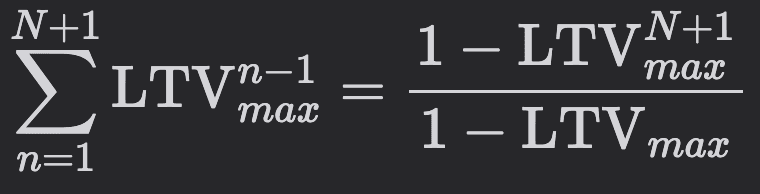

Where maximal leverage after N supply-borrow loops is defined as:

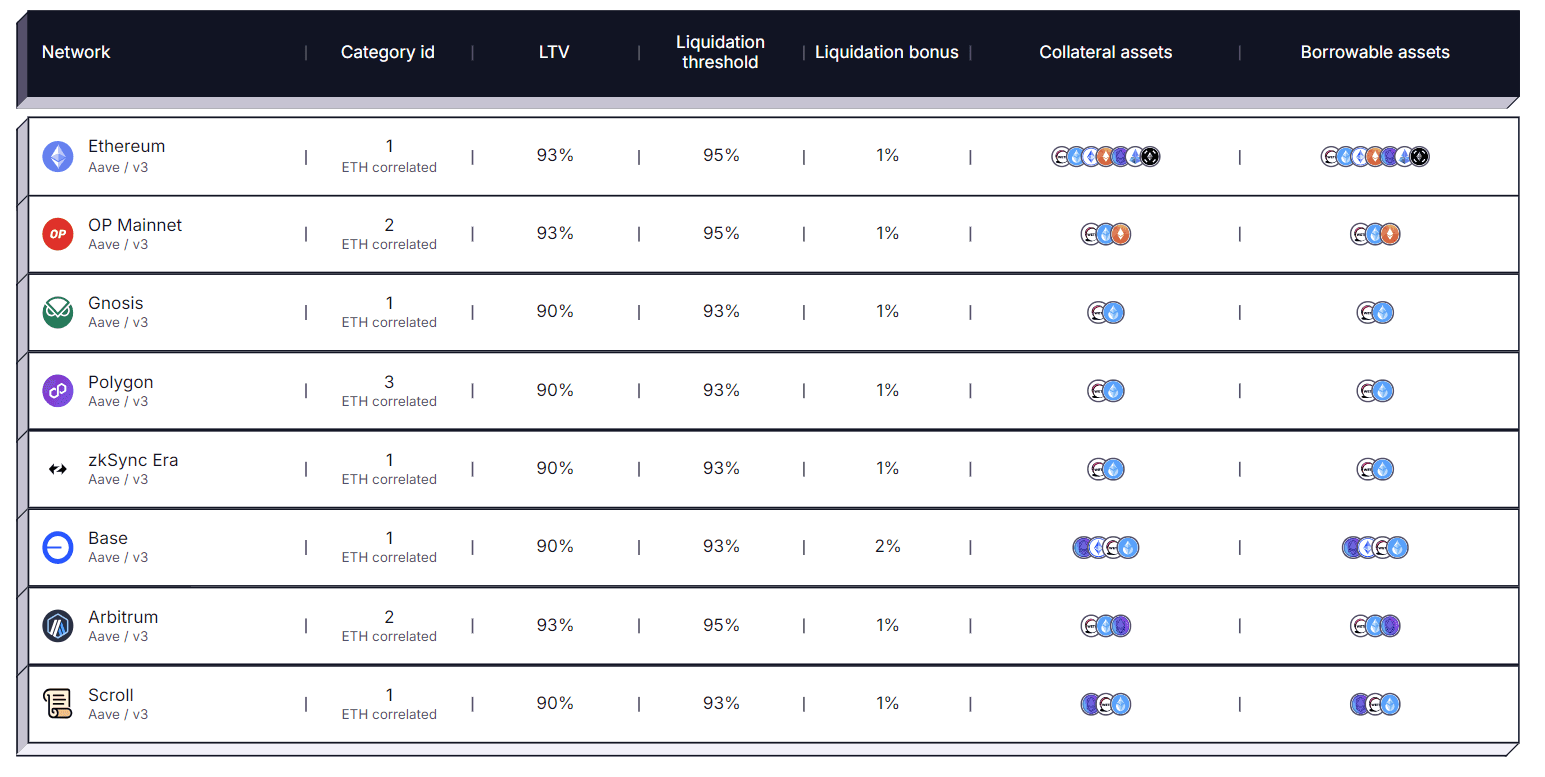

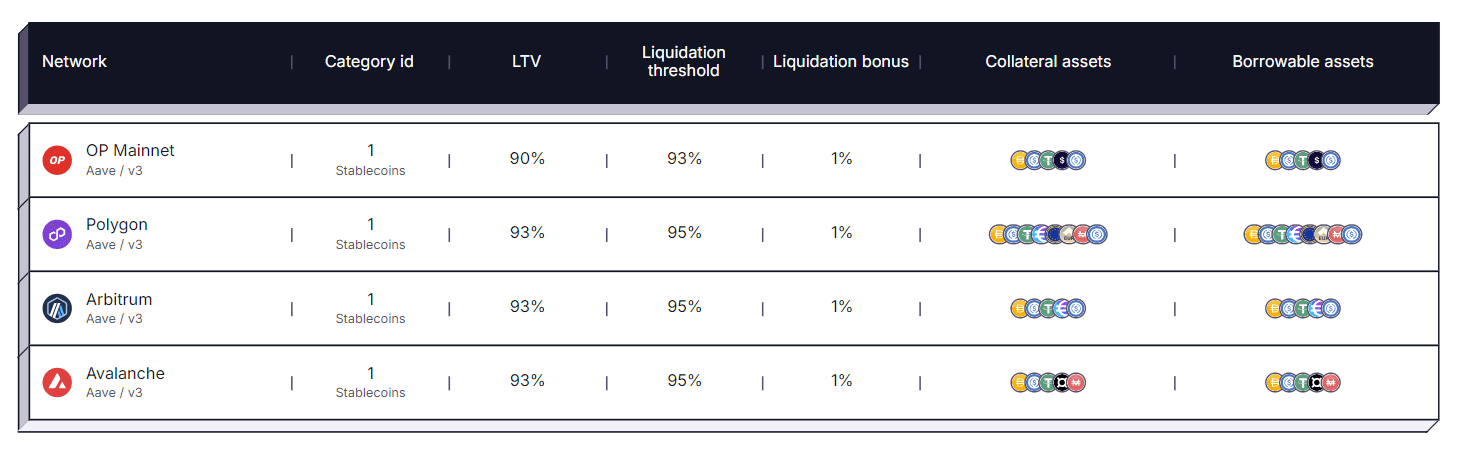

E-Modes could be deployed on all Aave market instances and could differ market-by-market. Until the introduction of liquid e-Modes, there were 2 main types of e-Modes: ETH-correlated and Stablecoins:

Source: Aave Dashboard

Chain-specific e-Modes exist across networks, such as AVAX Correlated e-Mode on Avalanche and MATIC Correlated e-Mode on Polygon. Each market's parameters are customized for local conditions - for instance, ETH Correlated e-Mode has a 90% LTV on Base versus 93% on Ethereum Mainnet, reflecting differences in liquidity and risk factors.

E-Mode has been successful across Aave deployments, especially in driving the adoption of ETH LST leverage strategies using assets like wstETH. While this success has led other DeFi lending protocols to adopt similar concepts, the original design had flexibility limitations. Aave introduced Liquid e-Modes to address these constraints and enable new possibilities.

#What is liquid e-Mode?

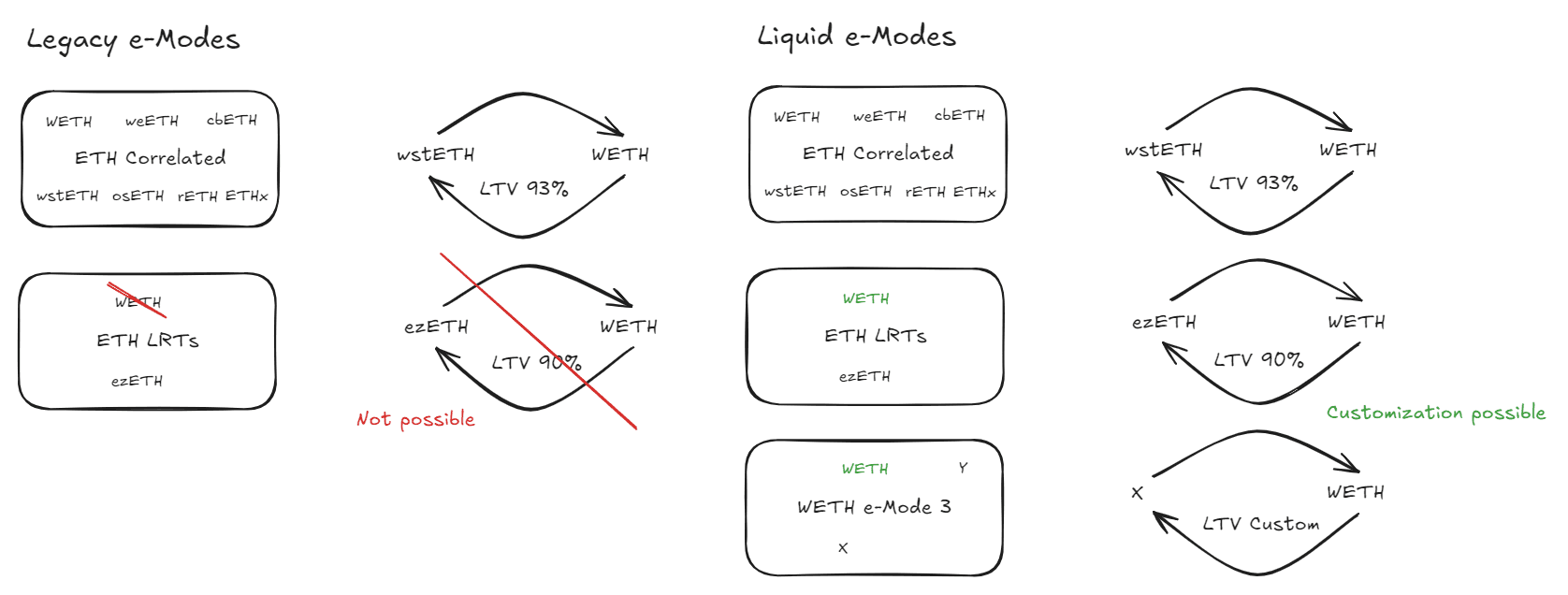

A key limitation of legacy e-Mode was that assets could not participate in multiple e-Modes simultaneously. For example, despite potential demand, WETH in ETH Correlated e-Mode couldn't be used in other e-Modes. This restricted users to scenarios like ETH LST supply-borrow looping, limiting WETH's utility in different configurations.

Liquid e-Mode removes this constraint, allowing assets to participate in multiple e-Modes. This will enable users to choose their preferred e-Modes and access more opportunities across Aave's markets.

Source: LlamaRisk

Liquid e-Modes allow assets to be flagged as borrowable, collateral, or both within an e-Mode. For example, in a wstETH/WETH e-Mode, wstETH could be set as collateral-only and WETH as borrowable-only to focus on wstETH leverage. In contrast, Stablecoins e-Mode configures all assets as both borrowable and collateral.

Legacy e-Modes were converted to liquid e-Modes with all assets set as both borrowable and collateral, ensuring existing e-Mode positions continued unaffected.

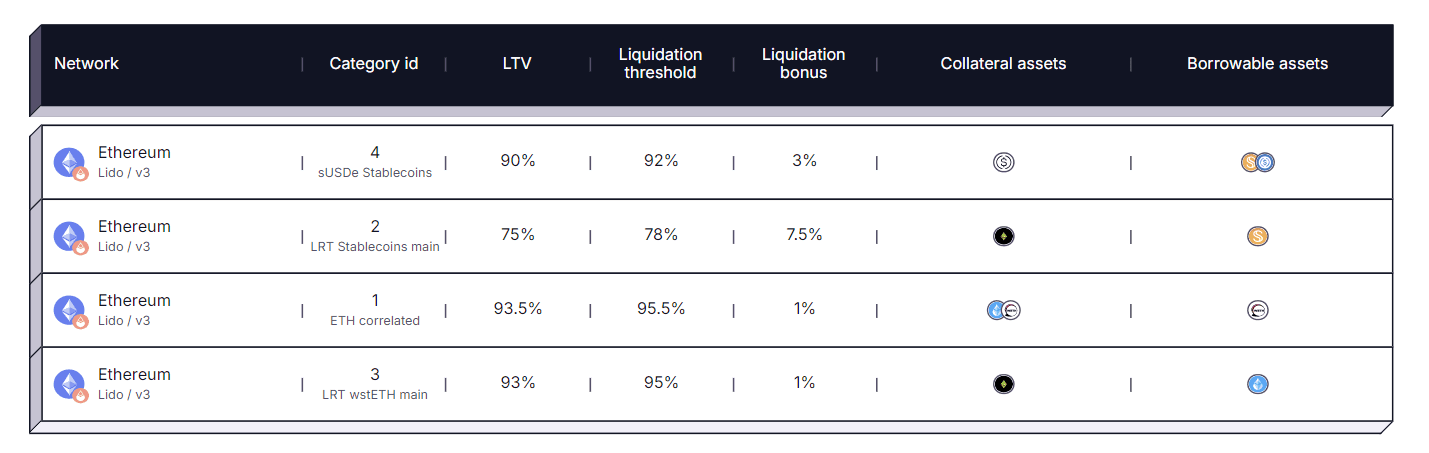

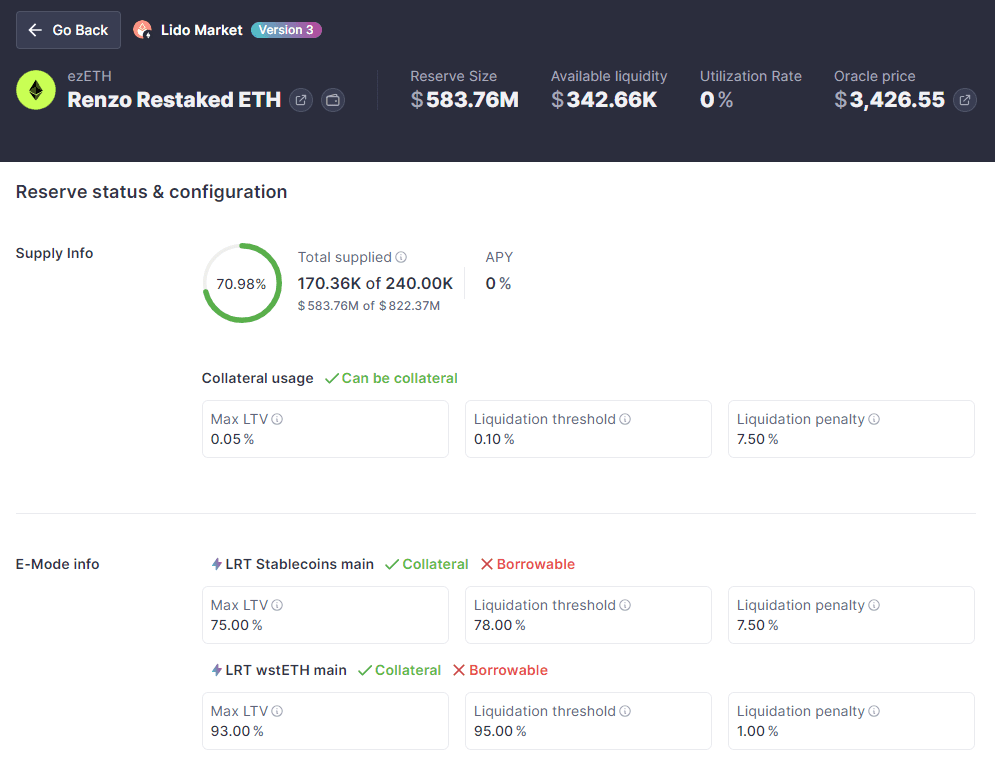

The update introduced several new liquid e-Modes, with the Aave Lido market serving as a pilot with 4 new configurations.

Source: Aave Dashboard

Ethereum Mainnet and BNB Smart Chain markets include new liquid e-Mode categories. The Lido market features:

-

sUSDe Stablecoins: Enables sUSDe yield leveraging through sUSDe supply and USDC/USDS borrowing. sUSDe is set as collateral, with USDC/USDS as borrow assets. Higher LTV/LT ratios are possible due to minimal price deviation between these yield-bearing stablecoins. Most effective when USDC/USDS borrow rates are low.

-

LRT Stablecoins: Uses ezETH LRT with 0 LTV/0 LT in regular mode, similar to isolation mode. The e-Mode allows borrowing specific stablecoins (USDS) using ezETH as collateral. Due to price uncorrelation, LTV/LT parameters remain conservative, matching regular borrow conditions.

-

LRT wstETH: Enables ezETH leveraging through wstETH borrowing only, offering higher LTV/LT for increased leverage—lower liquidation risk due to price correlation between ezETH and wstETH.

-

ETH Correlated: Modified standard ETH Correlated e-Mode where LSTs cannot be borrowed, focusing on LST yield looping and ETH exposure leveraging. Offers 0.5% higher max LTV than Ethereum Mainnet's ETH Correlated e-Mode.

{kind=link}

Source: ezETH regular vs. e-Mode parameters on Lido. - Aave

In light of the success of current liquid e-Modes, multiple new Aave governance proposals have been presented, offering to expand liquid e-Mode availability in various use cases and markets.

#What are the benefits?

Using liquid e-Modes will result in higher capital efficiency levels for users, enhancing the overall borrow utility of diverse assets. In turn, this should generate outsized additional revenue for the protocol relative to the increase in risk. Moreover, liquid e-Modes allow for more flexibility and offer multiple new solutions:

-

Liquidity Unification between otherwise separate market instances, where certain assets previously couldn't coexist due to competition for the same liquidity. For example, liquid e-Modes are necessary for ezETH and wstETH to compete for WETH liquidity, creating inefficiencies and suboptimal user experiences. Liquid e-Modes address this by isolating assets within specific configurations, enabling ezETH to contribute to wstETH supply yield (and indirectly to WETH supply yield). This approach fosters synergies rather than competition, ensuring smoother interactions. All of this has also allowed for Aave Instances Strategy Shift, where Lido and EtherFi market instances are planned to be merged.

-

Soft Onboarding of new assets, offering more flexibility in isolation. For instance, ezETH can be introduced with 0 LTV and 0 LT in regular mode, ensuring it does not affect overall protocol risk. Liquid e-Modes enable supply and borrowing use cases exclusively within specific configurations, achieving the same objectives as isolation mode but with a more customized selection of borrowable assets.

-

Explicit Push-and-pull Incentives to incline users to engage in specific supply/borrow patterns that were not as attractive prior. Examples of that could be the proposed tBTC/WBTC and cbBTC/WBTC Liquid e-Modes promoting borrowing of WBTC and subsequently larger leverage.

-

Custom LST/LRT Leverage Looping categories tailored to optimize utility while maintaining robust risk measures. For instance, the wstETH liquid e-Mode enables leverage strategies for ezETH, maximizing efficiency and yield for these token groups.

-

Yield-bearing Stablecoin Looping categories are designed to enhance leverage opportunities and maximize returns for price-correlated stablecoins. As outlined earlier, an example is the sUSDe liquid e-Mode, which focuses on stablecoin pairs to provide higher leverage and increased yield potential.

These and potentially more applications of the new version of e-Mode increase the number of debt assets used to power these trades and generate a potential to maximize efficiency for specific borrowing strategies. This grows TVL and boosts the revenue for Aave, which is a strong positive for the protocol.

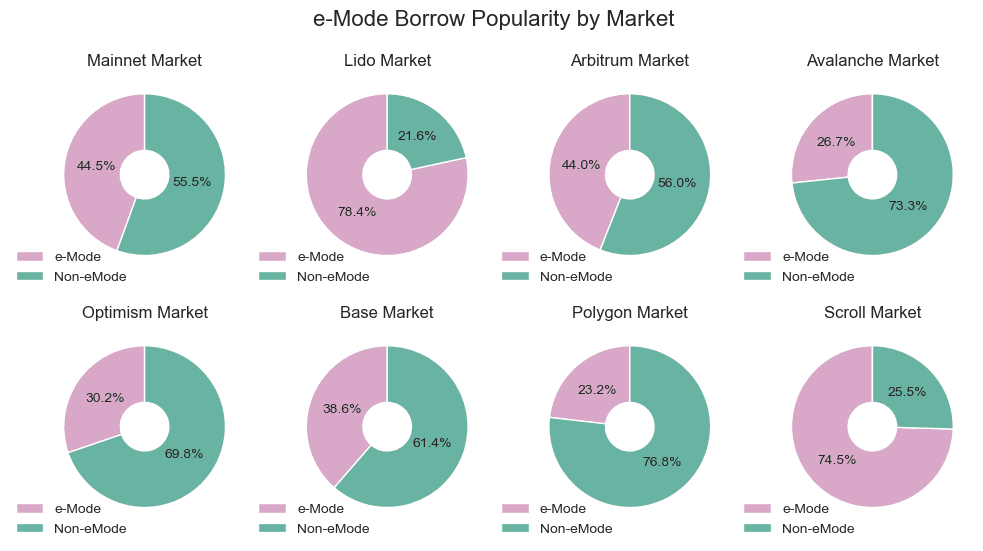

When comparing the borrow volume composition across various Aave markets, it is clear that e-Modes play a vital role in Aave's overall success. The effectiveness of e-Modes is particularly evident in the Lido market, where the use of liquid e-Modes is highly efficient, and in the Scroll market, where ETH leveraging is a key component driving the market's activity.

Source: LlamaRisk

#What are the risks involved?

The main incremental risk introduced by liquid e-Modes is that users may become more vulnerable to liquidation, given the more generous loan-to-value (LTV) parameters applied across a wider range of assets. While this risk also exists in the legacy e-Mode system, the interconnected nature of liquid e-Modes increases the potential for users to borrow against a broader range of collateral, enhancing capital efficiency. This broader borrowing scope may lead to more complex debt structures, increasing the likelihood of liquidation. While liquidations themselves do not directly threaten the protocol, large liquidation events during periods of high volatility could impact depositor capital.

However, this additional risk is mitigated by governance, which gates e-Modes to like-asset pairs, significantly reducing the likelihood of price deviations among assets within the same e-Mode. These markets are highly tailored to specific use cases (e.g., leveraged Ethereum staking), making them more stable. Nonetheless, users should know the risks inherent to different asset types, such as the de-peg risk for yield-bearing stablecoins or consensus penalty risk for ETH LSTs.

Nonetheless, depositors typically aim to avoid liquidation due to the penal premium they must pay. As noted, many borrowers tend to be risk-averse and avoid borrowing at maximum LTV ratios. Aave's risk providers continuously monitor changes in liquidity and borrowing composition to ensure the system remains stable.

#Conclusion

The introduction of Liquid e-Modes marks another point of progress in Aave's approach to optimizing capital efficiency while maintaining a robust risk management framework. By allowing assets to participate in multiple e-Modes, Aave has unlocked more flexibility for users, enabling them to pursue diverse strategies to maximize returns and optimize their positions. With Liquid e-Modes already demonstrating strong demand on platforms like the Lido instance, the feature has clearly shown its fit within the Aave ecosystem.

The expansion of Liquid e-Modes is poised to open up even more opportunities for users to engage in attractive risk-reward strategies. As more use cases and markets are incorporated, the potential for customized leverage, yield-enhancing strategy, and liquidity unification will continue to grow, further strengthening Aave's position in DeFi lending.